AMX CCF – Veritas – Global Focus

Veritas Funds plc

Article 10 SFDR Website Disclosure in respect of (the “Sub-Fund”)

1 January 2023

Regulation (EU) 2019/2088 on sustainability-related disclosures in the financial services sector, as amended (“SFDR”) requires certain EU-regulated entities (including Veritas Funds plc, the “Company”) to disclose information on a public website regarding the promotion of environmental and/or social characteristics for certain financial products.

This document (hereinafter referred to as the “Article 10 Statement”) constitutes the transparency disclosure with respect to the Sub-Fund for the purposes of Article 10 of SFDR and is available at the following website: https://www.vamllp.com/sustainability

This Article 10 Statement should be read in conjunction with the latest prospectus of the Company (the “Prospectus”) and the supplement in respect of the Sub-Fund (the “Supplement”) which sets out in detail the investment policy of the Sub-Fund and its approach to sustainable investment. The Supplement also incorporates the Annex setting out certain prescribed pre-contractual disclosures required under SFDR (the "Sustainability Annex").

Any capitalised terms appearing in this Statement and not expressly defined herein shall have the meaning given to them in the Prospectus and / or the Supplement.

Summary

This summary section has been completed in furtherance of SFDR and, in particular, Article 25 of Commission Delegated Regulation (EU) 2021/1288 ("SFDR Level 2") and summarises the key information referred to in the remaining sections of this Article 10 Statement.

Classification

The Sub-Fund has been classified a fund which promotes environmental and/or social characteristics under Article 8 of SFDR.

No Sustainable Investment Objective

The Sub-Fund promotes environmental or social characteristics in accordance with Article 8 of SFDR, but does not have a sustainable investment objective as contemplated by Article 9 of SFDR .

Environmental or social characteristics of the financial product

- The Sub-Fund seeks to promote both environmental and social characteristics.

- The environmental characteristics promoted by the Sub-Fund include a low carbon economy, reduction of greenhouse gas, and achieving Net Zero emissions.

- The Sub-Fund seeks to promote investment in companies that have a strong corporate sustainability practice in the following areas: Human Rights, Labour, Environment and Anti-Corruption. Assessments are consistent with global norms frameworks including the United Nations Global Compact (“UNGC”) and the United Nations Guiding Principles on Business and Human Rights ("UNGP").

- The Sub-Fund also seeks to promote societal and environmental characteristics by preventing the flow of capital from the Sub-Fund to issuers which have a significant exposure to controversial weapons as outlined in further detail below.

Investment Strategy

The Sub-Fund is designed for long-term investors who wish to build capital over a number of years through investment in a focused portfolio of global companies. The Sub-Fund is actively managed and is not managed in reference to, or constrained by, any benchmark. The Sub-Fund principally invests in equities, irrespective of specific geographical location listed or trade on Recognised Exchanges throughout the world. Investments may also be made in fixed income securities which are listed or traded on a Recognised Exchange, subject to the Investment Restrictions listed in the Prospectus, although it is not the current intention that such investments will be made. The Sub-Fund will not invest in leveraged notes. No consideration will be given to country or global index weightings, nor will the Sub-Fund be always fully invested in equities, and as a result, performance may be significantly different from that of the markets in which it is invested, or the performance of commonly followed global indices. Investments in the Sub-Fund may include financial derivative instruments, provided that such use does not materially alter the risk profile of the Sub-Fund.

Each target company is evaluated for its management of systemic sustainability risks such as climate change and corporate sustainability matters as described in the Supplement. The Investment Manager will integrate traditional environmental, social or governance ("ESG") factors into the analysis. All companies held are subject to the Investment Manager's ESG Voting Policy. Investee companies are also subject to a Net Zero Alignment Policy.

Proportion of investments

The Investment Manager intends to invest a minimum of 60% of the Sub-Fund's NAV in investments which attain the environmental and/or social characteristics promoted by the Sub-Fund. The remaining 40% of investments will be in investments which seek to achieve the broader objectives of the Sub-Fund, including those which may not match the Sub-Fund’s ESG criteria in its entirety or which are used for efficient portfolio management, hedging or liquidity management purposes as described in further detail below.

Monitoring of environmental or social characteristics

The Investment Manager's portfolio management team will implement the various criteria set out in this Article 10 Statement in making investment decisions. The Investment Manager's compliance function will monitor the integration of ESG requirements through a combination of automated, manual and periodic reviews.

Methodologies

Alignment is measured by identifying whether a company has either identified, or committed to identifying, a Science-Based Net Zero Target, or pledges to the Business Ambition for 1.5 °C campaign, each as categorised by the Science Based Targets Initiative (the "SBTi") as described in further detail herein. The emissions produced by the underlying investments held in the Sub-Fund are managed in line with the Investment Manager's commitment to achieving Net Zero by 2050 across the range of target companies in which it invests. The Investment Manager will also have regard to the carbon footprint and Weighted Average Carbon Intensity of an issuer, its alignment with the UNGC and UNGC, the exclusion of issuers with significant exposure to controversial weapons and the results of the principal adverse impact analysis described further in this document.

Data sources and processing

Data sources used to attain environmental or social characteristics promoted may include both proprietary information and third party data providers as described in further detail below.

Limitations to methodologies and data

Whilst it is recognised that data availability may impact the extent to which environmental or social characteristics promoted can be measured, this is managed through the use of both proprietary data and data sourced from third party data providers generally with broad capabilities and coverage.

Due diligence

Integration of ESG requirements is monitored through a combination of automated, manual, and periodic reviews. The data used to measure alignment is obtained from globally recognised sources. A report confirming the Sub-Fund’s adherence to the sustainability indicators is periodically provided to the compliance function.

Engagement policies

The VAM LLP Engagement Policy is available via the following weblink; https://www.vamllp.com/sustainability/

Designated reference benchmark

The Sub-Fund does not have a ‘Designated reference benchmark’ to attain the environmental or social characteristics promoted.

Introduction

This Article 10 disclosure document sets out information in relation to the sustainable investment approach of the Sub-Fund in accordance with the requirements of Articles 23 to 36 of SFDR Level 2. The headings below are in the order mandated by SFDR Level 2 and the information included beneath each heading address the prescribed information to be provided to investors pursuant to the above Articles.

As further described below, the Sub-Fund promotes, among other characteristics, certain environmental or social characteristics, provided that the companies in which investments are made follow good governance practices, in particular regarding sound management structures, employee relations, remuneration of staff and tax compliance.

No Sustainable Investment Objective. (Article 26: SFDR Level 2)

The Sub-Fund promotes environmental and/or social characteristics as set out below, but does not have a sustainable investment as its objective.

The Sub-Fund does not commit to making sustainable investments within the meaning of Article 2(17) of SFDR.

Environmental or Social Characteristics promoted by the Fund. (Article 27: SFDR Level 2)

The primary characteristic that the Sub-Fund promotes is a transition to a low carbon economy, which includes investment in businesses having a robust strategy in reducing greenhouse gas (GHG) emissions, a goal of achieving Net Zero, and science-based targets that illustrate how they intend to accomplish this goal.

Alignment is measured by identifying whether a company has either identified, or committed to identifying, a Science-Based Net Zero Target, or pledges to the Business Ambition for 1.5 °C campaign, each as categorised by the SBTi. The SBTi is a partnership between CDP (a global non-profit entity and climate research provider), the United Nations Global Compact (UNGC), World Resources Institute (WRI) and the World Wide Fund for Nature (WWF) which provides a process which allows participants to propose and receive independent verification of a commitment to reduce emissions in line with the Paris Agreement goals. This approach supports the UN Sustainable Development Goal 13 (Climate Action). The emissions produced by the underlying investments held in the Sub-Fund are managed in line with the Investment Manager's commitment to achieving Net Zero by 2050 across the range of target companies in which it invests. While the Sub-Fund has regard to SBTi categorisations, it may as the market evolves, elect at a future stage to have regard to an equivalent categorisation or rating provided by other entities which are widely used and which provide an equivalent assessment mechanism. In such an event any references herein to the SBTi or its categorisations shall be updated accordingly.

The Sub-Fund seeks to promote investment in companies that have a strong corporate sustainability practice in the following areas: Human Rights, Labour, Environment and Anti-Corruption. Assessments are consistent with global norms frameworks including the United Nations Global Compact (“UNGC”) and the United Nations Guiding Principles on Business and Human Rights ("UNGP").

The Sub-Fund also seeks to promote societal and environmental characteristics by preventing the flow of capital from the Sub-Fund to issuers which have a significant exposure to controversial weapons as outlined in further detail below.

Investment Strategy and Information on how environmental and social characteristics are met. (Article 28: SFDR Level 2)

The Sub-Fund is designed for long-term investors who wish to build capital over a number of years through investment in a focused portfolio of global companies. The Sub-Fund is actively managed and is not managed in reference to, or constrained by, any benchmark.

The Sub-Fund principally invests in equities, irrespective of specific geographical location listed or trade on Recognised Exchanges throughout the world. Investments may also be made in securities (including convertible bonds with equity linked notes which bonds shall be fixed and /or floating rate and shall generally be investment grade) which are listed or traded on a Recognised Exchange, subject to the Investment Restrictions listed in the Prospectus, although it is not the current intention that such investments will be made. The Sub-Fund will not invest in leveraged notes. No consideration will be given to country or global index weightings, nor will the Sub-Fund be always fully invested in equities, and as a result, performance may be significantly different from that of the markets in which it is invested, or the performance of commonly followed global indices. Investments in the Sub-Fund may include financial derivative instruments. Such instruments may be used to obtain, increase, or reduce exposure to underlying assets and may create leverage; therefore, their use may result in greater fluctuations of the Net Asset Value of the Sub-Fund. The Investment Manager will ensure that the use of derivatives does not materially alter the risk profile of the Sub-Fund.

Research that is conducted prior to the investment, includes a comprehensive sustainability analysis centred around the governance of the target company, which covers the following areas: demand and growth, business model, capital structure, board, executive remuneration, shareholder alignment, and capital allocation. These are issues that have the most potential to affect the company's ability to create value for shareholders. For example, it is important to ascertain if the target company engages in an activity that may adversely impact the sustainability of its operation or demonstrates a lack of vision to adapt.

The promotion of environmental and social characteristics is demonstrated throughout the investment process. Pre-investment, each company is evaluated for its management of systemic risks such as climate change and corporate sustainability matters that include human rights, labour, environment, and anti-corruption. The materiality of the related risks and opportunities will differ from company to company. The Investment Manager will complete in-depth research on any areas deemed material to the investment thesis, which will include assessing the impact over multiple time horizons and integrating traditional environmental, social or governance ("ESG") factors into the analysis at all steps of the process. Where it is deemed necessary, the potential impacts may be factored into the financial model and valuation of the business by the Investment Manager.

Post-investment, the Investment Manager will continue to monitor any changes impacting the abovementioned areas. Furthermore, all companies held are subject to the Investment Manager's ESG Voting Policy. If this voting policy guidance is breached, the Investment Manager will engage and /or vote against management to the extent required. Investee companies are also subject to a Net Zero Alignment Policy, whereby the Investment Manager expects companies within the Sub-Fund's portfolio to have committed to a Net Zero goal that is, at a minimum, consistent with the pledges made by the country of domicile, preferably by 2050.

The Investment Manager will also consider the application of carbon metrics such as carbon footprint (the total amount of greenhouse gases generated by the company normalised by market value) and the Weighted Average Carbon Intensity (a measure of carbon emissions normalized by revenues) which enable an assessment of emissions on an absolute and intensity basis. The Sub-Fund may invest in companies that may not be deemed to be aligned with a low carbon economy;

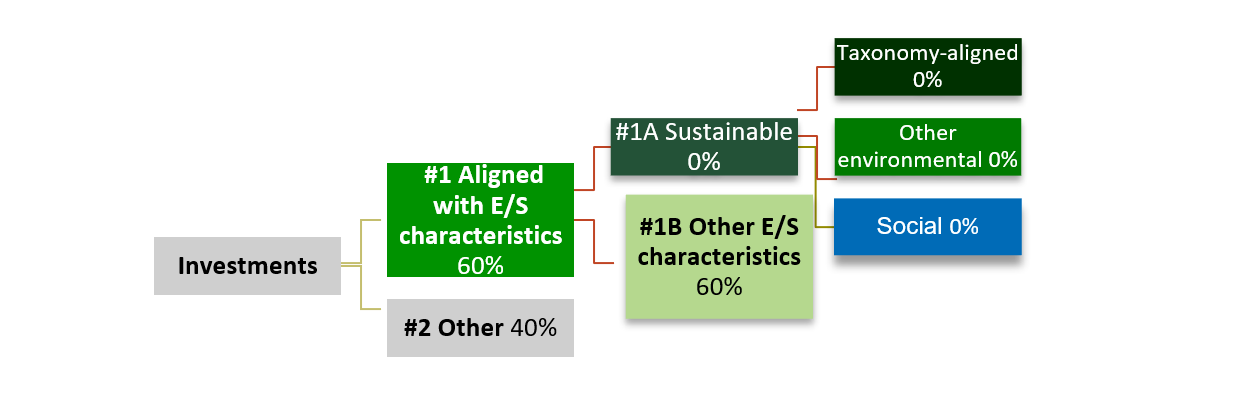

What proportion of investments are applied towards the promotion of environmental or social characteristics? (Article 29: SFDR Level 2)

The asset allocation is a by-product of stock selection with geographical and sector weight determined by the stocks bought. Given the valuation discipline of the approach, stocks are only purchased at the desired price, with cash levels rising and falling depending on availability of investment opportunities. A portion of the cash may be deployed into money market instruments.

#1 Aligned with E/S characteristics: The Investment Manager intends to invest a minimum of 60% of the Sub-Fund’s assets in investments which attain the environmental or social characteristics promoted by the portfolio. The figure stated will be reviewed periodically with the intention to increase the allocation to issuers with environmental and/or social characteristics as underlying companies adopt policies and procedures that allows the Investment Manager to evidence that such underlying companies meet minimum criteria. The figure stated is deemed appropriate at the time of writing.

#1A Sustainable: The Investment Manager does not commit to invest a minimum percentage of the Sub-Fund’s assets in sustainable investments. Accordingly, the Investment Manager does not make any further minimum commitment to allocate sustainable investments among the sub-categories of Taxonomy-aligned environmentally sustainable investments, other environmentally sustainable investments, or socially sustainable investments.

#1B Other E/S characteristics: This sub-category covers investments aligned with the environmental or social characteristics that do not qualify as sustainable investments. Accordingly, the entire 60% of assets which attain the environmental or social characteristics in category #1 above shall be regarded as meeting other environmental or social characteristics but which do not meet the threshold requirements to be regarded as sustainable investments (for example, they have not been assessed against the 'do no significant harm' test necessary to qualify as a sustainable investment).

#2 Other: The remaining 40% of investments will be in investments which seek to achieve the broader objectives of the Sub-Fund, including those which may not match the Sub-Fund’s ESG criteria in its entirety or which are used for efficient portfolio management, hedging or liquidity management purposes as described in further detail below.

The intended minimum alignment with environmental and social characteristics of 60% set out in this section has been calculated based on a blended calculation which applies equal weighting to each of the binding elements used to select investments with environmental or social characteristics (being (a) the commitment to Net Zero, which must be met by a minimum of 30% of the companies in which the Sub-Fund invests, (b) the application of the exclusion list, which means that 100% of the companies in the Sub-Fund will promote a social and/or environmental characteristic by not having any exposure to controversial weapons and (c) the management of the Sub-Fund to achieve an overall carbon footprint which is 50% lower than that of the MSCI World (Net Dividends Reinvested) Index and which the Investment Manager believes will require at least 50% of the Sub-Fund to promote environmental characteristics by having significantly lower carbon emissions, calculated by reference to market value, than the comparable median carbon emissions figure for issuers within the index).

The Investment Manager will revisit the percentages set out above, and where appropriate, increase the percentages as market conditions evolve and a higher proportion of issuers make their own binding commitments to one or more of the criteria assessed by the Sub-Fund.

The table below illustrates the intended allocation.

How are the environmental and social characteristics and the sustainability indicators used to measure the attainment of each of those characteristics monitored over the lifecycle of the Fund? (Article 30 SFDR, Level 2)

The Investment Manager's portfolio management team will implement the various criteria set out in this Article 10 Statement in making investment decisions. Integration of ESG requirements is monitored through a combination of automated, manual, and periodic reviews. Portfolio alignment with Net Zero is monitored using data from the SBTi, which as outlined above, and provides a process which allows participants to propose and receive independent verification of a commitment to reduce emissions in line with the Paris Agreement goals. The data used to monitor Sub-Fund alignment with the Carbon Footprint target relative to the index, and issuer involvement with Controversial Weapons, is sourced from the third-party data provider, MSCI ESG Research. A report confirming the Sub-Fund's adherence to the sustainability indicators is provided to the compliance function periodically. This data report integrates a mechanism to alert the Investment Manager's compliance function where individual holdings, or the portfolio, are nearing any pre-determined thresholds in respect of the Sub-Fund. The compliance function will use the outputs of this report to engage with the portfolio management team with a view to ensuring that the Sub-Fund operates within the relevant sustainability indicators and thresholds set out in this document.

What are the methodologies used to measure how the environmental and social characteristics promoted by the Fund are met? (Article 31: SFDR Level 2)

A number of metrics are utilised to measure the manner in which the environmental and social characteristics promoted by the Sub-Fund are met.

To meet the environmental and social characteristics promoted, the Investment Manager combines an assessment of ESG risks and opportunities with an exclusion criterion to act as the binding elements considered part of the Sub-Fund’s investment strategy.

- The Sub-Fund will ensure that a minimum 30% of net assets are invested in companies committed to achieving Net Zero. Compliance will be measured using verification and commitments aligned with Science-Based Net Zero Target methodologies and/or pledges to the Business Ambition for 1.5 °C campaign, each as promoted by the SBTi.

- A set of fixed exclusion criteria is in place to exclude companies or issuers from consideration for investment where their revenue is significantly derived from controversial weapons (for example. anti-personnel mines, cluster munitions, chemical weapons, and biological weapons).

- The Sub-Fund will be managed to achieve an overall carbon footprint (calculated with regard to Scopes1+2) that is a minimum of 50% lower than that of the MSCI World (Net Dividends Reinvested) Index.

- The Investment Manager may also consider the application of carbon metrics such as carbon footprint and the Weighted Average Carbon Intensity which enable an assessment of emissions on an absolute and intensity basis. The Sub-Fund may invest in companies that may not be deemed to be aligned with a low carbon economy.

- The Investment Manager will revisit the percentages set out above, and where appropriate, increase the percentages as market conditions evolve and a higher proportion of issuers in target markets make their own binding commitments to Net Zero initiatives.

Use of certain Principal Adverse Impact indicators

The Investment Manager is not obliged to consider principal adverse impacts on sustainability factors ("PAIs") under SFDR as it is not subject to the entity level reporting requirements under Article 4 of SFDR and the Sub-Fund does not commit to invest in companies classified as sustainable investments (which would require a full PAI review as part of the "do no significant harm" test). However, the Investment Manager has determined to have regard to the relevant PAIs set out in Annex I of the regulatory technical standards ("RTS") published by the Commission in furtherance of SFDR (Commission Delegated Regulation (EU) 2022/1288) as a mechanism to allow it to consider any negative external effect of its investments on environmental and social characteristics, including the transition to a low carbon economy and achievement of Net Zero emissions.

In that context, six of the PAIs have been deemed relevant to the Sub-Fund, being: 1. GHG emissions, 2. Carbon footprint, 3. GHG intensity of investee companies, 4. Exposure to companies active in the fossil fuel sector, 10. Violations of UN Global Compact principles and Organisation for Economic Cooperation and Development (OECD) Guidelines for Multinational Enterprises and 14. Exposure to controversial weapons (anti- personnel mines, cluster munitions, chemical weapons, and biological weapons).

For the majority of PAIs, the data used to assess these items is reviewed annually for each business, except for PAI 10, where the global norms principles are monitored more frequently, and reporting is provided to the investment team should any issues arise.

In terms of climate related PAIs, an assessment of the target company’s progress is made pre-investment, including an evaluation of the company’s climate strategy. The assessment criteria incorporates the 4 pillars of the Taskforce on Climate Financial Disclosures framework (TCFD) being (i) governance, (ii) strategy, (iii) risk management, and (iv) metrics and targets.

Post-investment, the Investment Manager shall continue to monitor these areas. If any shortfalls are identified, the Investment Manager shall engage with management to verify whether any steps are being taken to improve PAIs. In instances where a systemic risk such as climate change is deemed a material risk to the investment thesis, the potential impacts may be factored into the financial model and valuation of the business with reference to sustainability aspects. If the risk is deemed material and it is not managed appropriately, or the relevant company has not responded appropriately to engagement and made verified steps to improve PAIs, the Investment Manager may disinvest from the business.

Information on the data sources used by to attain the environmental and/or social characteristics promoted by the Fund. (Article 32: SFDR Level 2)

The Investment Manager’s ESG analysis is conducted in-house with full integration within its investment process. At present, a variety of data sources are utilised: MSCI ESG Manager Research (ESG research and analytics platform); Institutional Shareholder Services ("ISS") (proxy advisory firm); Carbon Disclosure Project (“CDP”) (a global non-profit entity and climate research provider); Sustainability Reports (annual reports published by the issuer); NGO Data including the Science Based Targets Initiative ("SBTi") (Independent body that verifies Science-based Carbon Reduction Targets), and Taskforce on Climate Financial Disclosures ("TCFD") (Reporting framework established by the Financial Stability Board (FSB)). The sources listed are utilised in reporting, monitoring, and to assist with guiding stewardship efforts. Where feasible, data available from multiple sources will be compared to ensure the use of the most recent information. The investment universe consists primarily of mid and large-cap stocks; therefore, coverage for the majority of data points is not an issue.

The range of data sources in relation to sustainable investing is evolving rapidly and the Investment Manager will review the above list in light of any new entrants who enter the market and/or changes in the range of services or data provided by existing data providers. This evaluation will take place on an informal basis over the operation of the Sub-Fund as the Investment Manager identifies new data sources entering the market. On an annual basis, the ESG Team will formally review third-party providers' data offerings to assess whether any data would be additive to the investment process and/or whether any improvements to client reporting could be made by using previously unavailable data.

What are the limitations to the methodologies and data sources used to evaluate the attainment of Environmental or Social characteristics? (Article 33: SFDR Level 2)

The methodology applied by ESG data providers is often inconsistent, with different providers and data sources choosing to emphasis certain factors over others, with the result that different data providers or data sources may have widely diverging views as to the environmental or social characteristics of a given issuer.

To assess company involvement in different activities, the Investment Manager and third-party data providers strive to obtain information directly from companies. Sources of data include annual reports, regulatory filings, sustainability reports, press releases, investor presentations, company websites, and other company disclosures. Industry databases are cross-referenced to complement company disclosures.

In terms of limitations of the data and the use of the data, measurements that involve snap shots, such as the principal adverse impact indicators, can have different reference timeframes. Due to point in time assessments of, for example, previous fiscal year revenues on an individual issuer, or statements made from such an issuer that has been subject to further qualitative analysis from a third-party provider, the calculation of the principal adverse impact indicators therefore results in a non-quantifiable margin of error. Lack of granularity in the data sources used in combination with using historical data published in, for example, annual reports means that there is both a significant time lag in snapshot metrics as well as challenges to data quality.

Carbon data is slightly different. Historically, company disclosure has been voluntary and data providers have developed proprietary methodologies to capture outliers and in cases of non-disclosed data to use estimates. Estimates facilitate portfolio level assessments, but limits accuracy of company level assessments. Carbon emissions data quality is essential to the calculation of carbon metrics and the use of estimates may affect aggregated portfolio level data.

Limitations to norm-based research and controversial weapons research are related to the differences in methodologies rather than lack of or quality of data as they use publicly known alleged or verified incidents or controversies, such as violation of labour rights reported in the media. Different research providers have different methodologies for collecting this type of information and for how that information is assessed. Where a company is reported as breaching a global norms principle, the Investment Manager's methodology includes reaching out to companies to get their view on the issue, any action plans, or other plans in relation to the controversy or any other relevant information.

Other limitations include a lack of ESG disclosure by issuers, a lack of data available from third-party providers on specific topics (such as biodiversity reporting), and a lag in the frequency with third-party providers publish updated ESG data points.

The Investment Manager has access to multiple sources, which ensures diversity of inputs and assists with the abovementioned issues. Furthermore, as the regulatory landscape and expectations around company disclosure become formalized, it is expected that the quality and accuracy of data will improve.

What due diligence is carried out on the underlying assets of the Fund? (Article 34: SFDR Level 2)

The Investment Manager believes ESG factors offer the most valuable insight when they sit within the framework of fundamental analysis, i.e., they are part of the overall assessment of quality and not a separate rationale or function. It becomes apparent on a case-by-case basis what material ESG factors need to be assessed. The aim is to look for high-quality companies and remain patient to buy these companies at the right entry point. The more predictable a company is, the easier it is to model, and the higher the likelihood of making the desired return. ESG integration can be demonstrated throughout the investment process.

The first part of the process, idea generation, is identifying high-quality companies to add to the investment universe. The analysts focus on a list of stocks that have been identified in a number of ways. These include 'themes'; some of the themes/trends that are focused, on have a clear environmental and social impact recognised by the management teams of the companies in which investments are held. The resulting short list of companies is those that initially look as if they may be attractive long-term investments and warrant further analysis. The appropriate analyst(s) will analyse the company in depth and, at this stage, include any consideration that may affect the sustainability of the business. Since management is core to this, management is assessed based on criteria that includes past/ present stewardship, management of expectations and, crucially, vision. How a company intends to deploy cash given its expectations over the next 10 years for the future prospects of their industry or sector is key.

In addition to the above, all target companies are formally monitored pre and post-investment for compliance with relevant international frameworks published by intergovernmental organisations, such as the United Nations, which set out expected behaviours in respect of business practices. The relevant frameworks include the UNGC and the UNGP. A third-party screen is run monthly on companies within the Sub-Fund's portfolio and target companies within the investment universe. The screen covers principles listed under the UNGC and the UNGP. The Investment Manager will identify any companies listed that are identified as having "Failed" the screen for non-compliance with the principles outlined under the Global Norms Framework listed above. The Investment Manager will assess the materiality of the violation and engage with the relevant issuer if necessary.

All companies held are subject to the Investment Manager's Voting Policy, which enforces a high standard of governance. If the Policy guidance is breached, the Investment Manager will engage and /or vote against management to the extent required.

Investee companies are also subject to a Net Zero Alignment Policy, whereby the Investment Manager expects companies within the Sub-Fund's portfolio to have committed to a Net Zero goal that is, at a minimum, consistent with the pledges made by the country of domicile, preferably by 2050 and, as part of the due diligence, the Investment Manager will document the relevant public commitment made by the issuer to justify its inclusion within the target percentage of companies with a Net Zero goal.

The Investment Manager shall review all target investments against the exclusion list of companies or issuers whose revenue is significantly derived from controversial weapons (for example. anti-personnel mines, cluster munitions, chemical weapons, and biological weapons).

The Investment Manager shall also consider the carbon emissions of individual issuers with a view to considering their impact on the overall portfolio and the binding criterion of ensuring that the overall carbon footprint of the Sub-Fund (calculated with regard to Scopes1+2) is a minimum of 50% lower than that of the MSCI World (Net Dividends Reinvested) Index. These reviews are completed using the various data sources outlined above.

What are the Engagement Policies pursuant in respect of investments made by the Fund? (Article 35: SFDR Level 2)

The Investment Manager considers itself an 'engaged owner' of the businesses into which it invests (not just shareholders who buy and sell shares). The Investment Manager is therefore willing and able to engage with companies to influence governance. Engagement is done actively and regularly with the companies and a constant dialogue on all key issues is maintained. These are issues that have the highest potential to affect the company's ability to create value for shareholders. Examples of engagement triggers are as follows: Action that is not aligned with shareholder interests and/ or deterioration in the quality of management; Breach of Voting Policy Guidance; Controversy flagged that breaches UN Global Compact ("UNGC"); and Task Force on Climate-related Financial Disclosures ("TCFD") shortfalls.

Tier 1 is defined as a specific attempt to influence governance/business practices that may have a material impact on long-term sustainable value creation. Tier 2 are proactive interactions with a company to promote good business practices. Environmental and social issues may be raised in both areas. Under Tier 1, material issues will differ from company to company and sector to sector. The investment manager will have an assessment from the original research on what is material for a business. If the company engages in an activity that challenges its operation's sustainability or demonstrates a lack of vision to adapt, we will have cause to engage.

Coupled with materiality, the investment manager has a part to play in encouraging constructive behaviour. Related to environmental factors, there is a policy to engage with management to publish climate-related disclosures even where it may not be seen as a material risk to the business.

An engagement log is kept that records the engagement objective, method of communication, a summary of dialogue, time frame for implementation of necessary changes, and next steps (if required e.g., voting against management, timeframe for follow-up engagements etc.).

Has any index been identified as a "designated reference benchmark" in order to meet with the environmental or social characteristics promoted by the Fund (Article 36: SFDR Level 2)

The Sub-Fund does not have a ‘Designated reference benchmark’ to attain the environmental or social characteristics promoted.